SMM7 March 10:

Review in June:

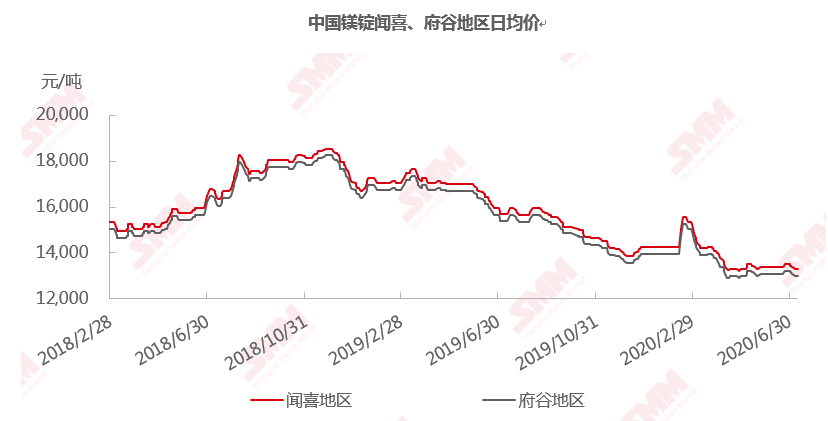

In June 2020, the average monthly price of magnesium ingots in Wenxi area is 13367.5 yuan / ton, and that in Fugu area is 13067.5 yuan / ton.

In June, the spot price of magnesium ingot is relatively stable as a whole, with only a small range of price fluctuations, which is not large and will not be maintained for a long time, and has not formed the mainstream rising and falling trend in the market. From June 1 to 22, the ex-factory price of magnesium in Fugu area is basically maintained at 13050 yuan / ton, while the mainstream transaction price of magnesium in Wenxi area is 13300 Mel 13400 yuan / ton. From June 23 to the end of the month, the price of magnesium ingots began to rise, but the range was limited, rising only 100 yuan / ton.

At the end of May, due to the bidding of downstream steel mills, the demand for ferrosilicon increased, while the ferrosilicon plant began to limit production and guarantee prices since March, the operating rate was insufficient, so the supply of ferrosilicon fell short of demand in a short period of time, and the price also continued to rise. Magnesium ingot producers in Youfugu said that the rise in ferrosilicon prices has caused certain cost pressure on the upper reaches of magnesium ingots, while the price of 13050 yuan / ton does not have much profit space, with the rise of the production cost line, the upper reaches are generally reluctant to continue to lower prices. Since June, the upstream production plants have accelerated the pace of maintenance, and many factories have begun maintenance plans one after another, some overhauling all production lines at once, and some taking turns overhauling to ensure the supply of magnesium ingots. According to SMM research, the inventory of upstream magnesium ingot production plants is limited. At present, several manufacturers in the market focus on 95B magnesium ingots, so 90 magnesium ingots are very few, so there is no inventory; and most of the other general magnesium producers also say that inventory is controllable or even out of stock, and there are more pre-sale orders, so the overall inventory pressure is not great. Sales staff in Fugu area said that in the case of rising ferrosilicon prices, the price of 13050 yuan / ton is no different from the previous lowest price of 12800 yuan / ton, although the current price remains unchanged, but for upstream factories, it is also equivalent to a price reduction in disguise, so even if the demand is sluggish, the upstream price attitude is still firm.

From the first ten days of June to the middle of June, the price of magnesium ingots is stable, but the overall trading volume of the market is not large, it is still dominated by downstream demand, the export situation has not improved, and the overall demand for magnesium ingots has shrunk, so prices lack the power to rise. The psychological price downstream is generally low, and there are many cases of price depression. according to magnesium ingot manufacturers in Fugu area, some demand downstream gives a purchase price of 13000 yuan / ton, but the upstream price is firm and refuses to sell below 13050 yuan / ton. therefore, the difference in psychological price also affects the transaction to a certain extent.

In late June, coal prices also began to rise due to the contraction in upstream supply, and the price of 75 ferrosilicon has also risen to 5800 yuan / ton. Affected by the rising prices of ferrosilicon and coal, upstream magnesium ingot factories began to raise magnesium ingot prices due to cost pressure. The overall quotation in the upstream began to be raised, because some factories had no inventory or little inventory pressure, and the price upward momentum was strong, with the highest quotation at 13500 yuan / ton, while the quotations of other factories were slightly lower for the purpose of clearing inventory or withdrawing funds. Most of them gradually increased from 13050 yuan / ton to 13200 yuan / ton. The price rise has a certain stimulating effect on downstream demand, superimposed near the Dragon Boat Festival holiday, some downstream also began to stock. As a result, trading volume has increased, but the increase is limited, and overall demand is still weak.

Future forecast: in July, as most of the downstream stock demand has been completed before the Dragon Boat Festival, there is no hurry to purchase more wait-and-see attitude, so the overall market transaction is weak, and the downstream price reduction is more serious, the downstream psychological price is generally low, the market demand is sluggish, the price lack of support is gradually declining, the upstream factory price is unable to passively reduce, and the possibility of price reduction is very high.

In terms of production, July will still be the peak period for upstream overhauling. Some factories have started overhauling since June, while others have overhauled all production lines at once and resumed normal production after overhauling. Some different production lines take turns overhauling to ensure adequate inventory. Some of the factories that have not been overhauled in June are scheduled to start overhauling in July, and the factories that have not been overhauled will also complete the overhaul in July. Upstream production of magnesium ingots will continue to reduce the supply of magnesium ingots in July, as the predictable reduction in downstream demand is considered to limit production and protect prices, so it is not wise to release production at this time.

On the demand side, the overall market turnover is weak, there is still no sign of improvement in July, or even worse than in June. Market turnover is still dominated by downstream demand, and there is no obvious change. Export orders for magnesium ingots have been severely reduced by the overseas epidemic, with only a small number of transactions in Japan, South Korea and Europe, and export orders from most producers have been delayed or cancelled. The demand of downstream magnesium powder and magnesium alloy processing plants has also decreased, on the one hand, it is also affected by product exports, on the other hand, due to the sales of end products and reduce the demand for raw materials. Most magnesium powder factories downstream said that July is the peak period for production and overhaul of pharmaceutical and chemical plants, which is usually overhauled for about a month, while pharmaceuticals and chemical industry are important consumers of magnesium powder downstream except steel mills, so the output of magnesium powder and magnesium chips will decrease significantly in July, reflecting that the demand for magnesium ingots will be reduced accordingly. According to SMM research, the orders of downstream magnesium alloy factories in July are not much different from those in June, but in the later stage, with the sales pressure of end products, the reduced demand for magnesium alloys will gradually be reflected in the raw materials.

SMM analysis, although the current price is basically close to the cost line of most upstream factories, and ferrosilicon, coal as magnesium ingot production raw materials recent prices are in a rising period, but the market transaction is not optimistic, upstream more negative sentiment, in the case of the overall demand predictability reduction in July, magnesium ingot prices are difficult to stabilize, there is a risk of continued decline, so it is expected that the domestic magnesium ingot price trend will fluctuate downwards in July.